What is the Contracted Rate?

The contracted rate is the amount of money the insurance company and provider have agreed to pay/be paid for the medical service.

In other words, it is the discounted amount patients with insurance are charged when seeing in-network providers.

The contracted rate is sometimes called the “allowed amount” or the “insurance allowed amount”.

Understanding the contracted rate

Each year, the insurance companies (ex. Cigna) and the healthcare providers (ex. Duke Healthcare) decide what their “discounted rate” or “allowed amount” is as an in-network provider.

For example:

*(Prices listed below are only an example, they are not real prices.)*

According to their chargemaster, Duke Hospital says they charge $5,200 for a breast MRI.

Cigna negotiates that because Duke is an “in-network provider” for their plans, their members will instead be charged a discounted, “contracted rate” of $2,100.

Cigna members will then receive a bill for the “contracted rate” of $2,100, applied to their benefits (usually a deductible).

Why does the contracted rate matter to me?

If you have insurance and are trying to determine what a procedure will cost you, knowing the contracted rate is essential to understanding your overall cost. People often call a hospital to ask what the cost of their procedure will be, and the hospital may only tell them the rate that they charge everyone, not the rate that is specific to your insurance plan.

It is also important to ensure that you have been billed the contracted rate, not the full price, if you have medical insurance. If you have insurance but receive a bill for the full price of a procedure, read this article about what to do if you get an unexpected medical bill.

Does every insurance company have the same contracted rate?

Every company has a different contracted rate with each provider. The contracted rate varies significantly from one insurance company to the next. BCBS, for example, may have a lower contracted rate for one procedure at one hospital, and a higher contracted rate for another procedure at the same hospital.

Who decides the contracted rate?

The contracted rates are usually negotiated and agreed upon in annual negotiations between provider groups and insurers.

How can I find the contracted rate at my hospital?

The best way to find out the contracted rate in advance of any procedure is by calling the hospital billing office and asking the following: “What is the contracted rate/allowed amount for procedure x with CPT code xxxxx with [insurance company name]?”

As of January 1, 2021, CMS is now requiring hospitals to list the contracted rates for 300 common “shoppable services” on their websites to help consumers access the information. Read this for an in-depth understanding of how to find procedure prices. (link to our latest article).

Some insurance companies have online cost estimators that may enable you to find the contracted rate, but the accuracy of those estimators varies widely.

What is an example of the contracted rate?

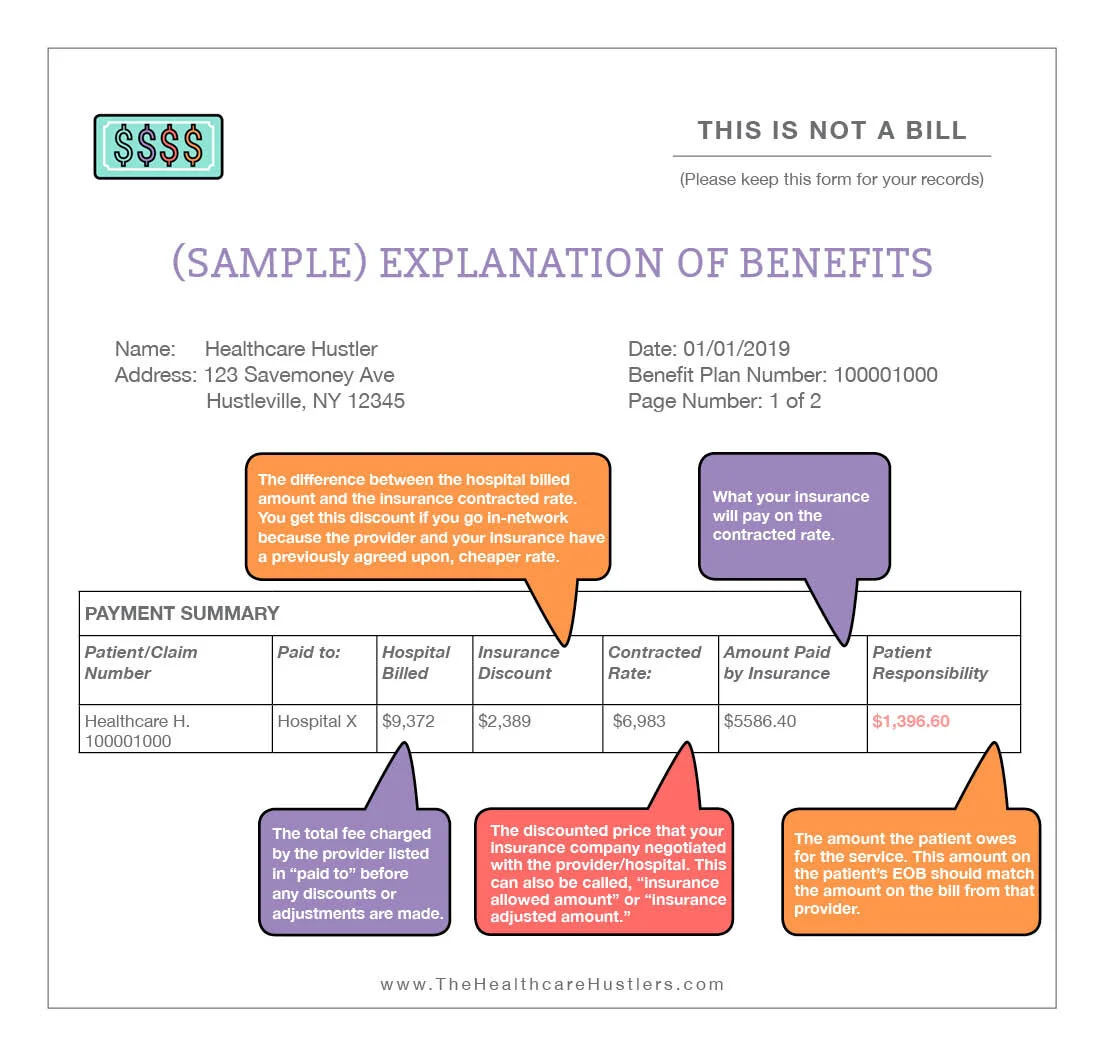

Devika is going to have a minor outpatient surgery at her local hospital. (Read this to see why there could be a cheaper option). The price listed on the hospital website’s chargemaster for that procedure is $9,372. Devika has insurance, and the facility is in-network with her carrier.

Because the facility is in-network, Devika will only pay her portion of the contracted rate (aka “the allowed amount”) - a price that the insurance provider and the hospital have previously agreed on.

Devika’s EOB will likely show the following:

Hospital billed: $9,372

The total amount for the facility fee (usually doesn’t include the doctor/physician fee)

Insurance Discount/Contracted Rate: $2,389

The difference between the hospital billed amount and the insurance contracted rate/allowed amount. In simpler words, the discount that you get because you are a BCBS/Cigna/Aetna/other insurer member.

Total amount owed after insurance discount: $6,983

AKA the contracted rate/the contractual rate/the allowed amount/the insurance allowed amount. In simpler words, the cheaper price that you get because you are a BCBS/Cigna/Aetna/other insurer member.

Insurance paid (80%): $5586.40

Assuming the patient had already met their deductible, and the contracted rate was then subject to 80%/20% coinsurance, as is common for facility charges.

Patient responsibility (20%): $1,396.60

Assuming the patient had already met their deductible, and the contracted rate was then subject to 80%/20% coinsurance, as is common for facility charges.

As you can see from this example, while the hospital website may say that the hospital charges $9,372 for the procedure, the actual patient responsibility is dependent on the contracted rate and the patient’s benefits.

Related Terms

PPO Plan vs High Deductible Health Plan (HDHP)

Relevant Articles

How to Understand the Cost of a Procedure

How to shop around for Outpatient Surgery

How to Understand the Explanation of Benefits